The Credit Card You Pick Can Save You Money

Smart consumers comparison shop for credit, whether they’re looking for a mortgage, an auto loan, or a credit card. Comparison shopping is important because it could save you money.

Credit Card Interest Rates

How Much Will You Pay?

Credit Card Shopper’s Checklist

Deciphering the Application

Glossary

For More Information

Survey

When you’re looking for a credit card, be sure to consider the costs and terms. They can make a difference in how much you pay for the privilege of borrowing. Compare them with the costs and terms of the cards you already have to find the plan that best fits your spending and repayment habits.

Key costs and terms to consider are the annual percentage rate (APR) for goods and services as well as for cash advances, the annual fee, and the grace period. Also compare cash-advance fees, late-payment charges, and over-the-limit fees.

Besides looking at these costs and terms, think about your typicalbill-paying behavior. Do you pay your outstanding balance in full each month? Or do you usually carry over a balance? Matching the credit card plan to your needs could save money.

Credit card issuers offer variable-rate, fixed-rate, and tiered-rate plans. For variable-rate credit card plans, the interest rate is calculated according to a formula. Three of the most commonly used formulas are

The most common indexes used by credit card issuers are the prime rate; the one-, three- and six-month Treasury bill rates; the federal funds rate; and the Federal Reserve discount rate. Most of the indexes are published in the money or business section of major newspapers. If the index rate used for your credit card changes, the rate on your card will, too.

The margin is a number of percentage points chosen by the credit card issuer. The card issuer also chooses the multiple.

The interest rate on a fixed-rate credit card plan, though not explicitly tied to changes in another interest rate, also can change over time. The card issuer must notify you before the “fixed” interest rate is changed.

A tiered interest rate means that different rates apply to different levels of the outstanding balance (for example, 16% on balances of $1 -$500; 17% on balances above $500).

Some card issuers may have a policy that raises your interest rate if you make late payments. For example, if you make 2 late payments within 6 months, the card issuer may raise your interest rate from 18%APR to 24% APR. If such a penalty rate applies to your card, the issuer must include a notice in the solicitation materials.

Card issuers may also charge different rates for different types of transactions. For example, the card may carry one rate for purchases of goods and services, another rate for cash advances, and still another rate for balance transfers.

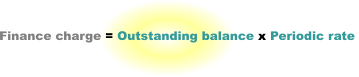

The finance charge–that is, the dollar amount you will pay to use credit–depends on your outstanding balance and the periodic rate in your credit card plan:

What Is the Outstanding Balance?

The outstanding balance can be calculated in several ways, and the method of calculation can make a big difference in the finance charge you will pay:

- Average daily balance method including new purchases. The balance is the sum of the outstanding balances for every day in the billing cycle (including new purchases and deducting payments and credits) divided by the number of days in the billing cycle.

- Average daily balance method excluding new purchases. The balance is the sum of the outstanding balances for every day in the billing cycle (excluding new purchases and deducting payments and credits) divided by the number of days in the billing cycle.

- Two-cycle average daily balance method including new purchases. The balance is the sum of the average daily balances for two consecutive billing cycles. One daily balance, that for the current billing cycle, is calculated by summing the outstanding balances for every day in the billing cycle (including new purchases and deducting payments and credits) and dividing that total by the number of days in the billing cycle. The other daily balance is that from the preceding billing cycle.

- Two-cycle average daily balance method excluding new purchases. The balance is the sum of the average daily balances for two consecutive billing cycles. One daily balance, that for the current billing cycle, is calculated by summing the outstanding balances for every day in the billing cycle (excluding new purchases and deducting payments and credits) and dividing that total by the number of days in the billing cycle. The other daily balance is that from the preceding billing cycle.

- Adjusted balance method. The balance is the outstanding balance at the beginning of the billing cycle minus payments and credits made during the billing cycle.

- Previous balance method. The balance is the outstanding balance at the beginning of the billing cycle.

Depending on the balance you carry and the timing of your purchases and payments, the average daily balance method excluding new purchases, the adjusted balance method, and the previous balance method tend to result in lower finance charges than the other balance-calculation methods.

What Is the Periodic Rate?

The periodic rate is the rate you are charged each billing period. Usually the periodic rate is the monthly interest rate, calculated by dividing the card’s APR by 12. If your card has different rates for different types of transactions, then different periodic rates will apply to those balances. For example, if your card has a 12% APR on purchases, the periodic rate for purchases is 1%; and if your card has a 24% APR on cash advances, the periodic rate for cash advances is 2%.

The Right Card for You

While the outstanding balance and the periodic rate are important factors in choosing a credit card, they shouldn’t be your only considerations. Other plan features may be more important to you, depending on how you use the card. For example, if you don’t always pay your monthly bill in full, you’ll probably be more interested in a card that carries a lower APR. On the other hand, if you always pay your monthly bill in full and card enhancements such as frequent flyer miles don’t interest you, your best choice may be a card that has no annual fee and offers a longer grace period.

The grace period is the number days between the statement date and the due date during which you can pay your bill without incurring a finance charge. The card issuer may refer to the beginning or ending point of the grace period and tell you about any conditions that apply. For example, the issuer may say you have “25 days from the statement date, provided you have paid your previous balance in full by the due date.” Keep in mind that the statement date is not the date on which you receive the bill; it is the date on which the issuer prepares the statement, which may be a week or two before you actually receive the bill in the mail.

How Much Could You Save?

The following example illustrates the annual savings you could achieve by switching to a credit card plan with a lower APR and no annual fee. The average monthly balance used in this simplified example is around the national average for consumers with credit card debt.

TermsPlan APlan B

| Average monthly balance | $2,500 | $2,500 |

| APR | x 18% | x 14% |

| Amount paid in finance charges annually | $450 | $350 |

| Annual fee | + $20 | + $0 |

| Total cost | $470 | $350 |

By switching to a credit card plan with a lower APR and no annual fee, you could save $120 annually. Of course, this example assumes that the interest rate is applied to a constant balance of $2,500 and that you make all payments on time; if you paid down some of the balance each month, the amount paid in finance charges annually would be less. Also, if you make a payment late, you may incur additional fees that will increase your cost.

Credit Card Shopper’s Checklist

Here are some tips for shopping for a credit card or evaluating the cards you already have.

- Make a list of features that best fit your needs, and rank them according to how you plan to use the card.

- Call the issuers of the cards that seem to match your needs to verify the publicized information. Ask if they have any other plans available.

- If you are currently a cardholder and have a good credit rating, ask the issuer of your card to lower your current rate or to reduce or waive your annual fee. Negotiate.

Review the following information about the plans:

Availability

Is the card accepted nationally? Regionally? Only in one state? Only in a specific store?

Interest rate pricing

Is the interest rate fixed? Variable? Tiered? If the rate is variable, what is the index? The margin? The multiple?

APR

What is the APR for purchases? For cash advances? For balance transfers? Is there a penalty rate if you make late payments?

Finance charge

What method for determining the outstanding balance is used to calculate the finance charge?

Annual fee

What is the annual fee, if any?

Grace period

What is the grace period for purchases? (Grace periods usually do not apply to cash advances, which begin accruing interest from the day of the transaction.)

Other features

Does the plan offer enhancements that are attractive to you, such as cash rebates, purchase protections, warranties or guarantees, travel accident or automobile rental insurance, discounts on goods and services purchased, and incentives for use, such as frequent flyer miles? Are these features available at no extra cost?

Deciphering the Information in a Credit Card Solicitation or Application

Certain key pieces of information must be included in all solicitations or applications for credit cards. Look for a box similar to the one below for information about interest rates, fees, and otherterms for the card you are considering.

| 2.9% until 11/1/00 after that, 14.9% | |

| Your APR for purchase transactions may vary. The rate is determined monthly by adding 5.9% to the Prime Rate ** | |

| 25 days on average | |

| Average daily balance (excluding new purchases) | |

| None | |

| $.50 | |

| Transaction fee for cash advances: 3% of the amount advanced Balance-transfer fee: 3% of the amount transferred Late-payment fee: $25 Over-the-credit-limit fee: $25 Explanation of penalty. If your payment arrives more than ten days late two times within a six-month period, the penalty rate will apply. The Prime Rate used to determine your APR is the rate published in the Wall Street Journal on the 10th day of the prior month. |

APR for purchases

The interest rate you will pay, on an annual basis, if you carry over balances on purchases from one billing cycle to the next. If the card has a temporary introductory rate, the rate that applies after the temporary rate expires is also stated.

Other APRs

The interest rates you will pay, on an annual basis, if you get a cash advance on your credit card, if you transfer a balance from another credit card, or if the card issuer applies penalty rates. (More information on the penalty rate may be included outside the disclosure box–for example, in a footnote.)

Variable-rate information

If the card has a variable rate instead of a fixed rate, this section will tell you how the variable rate is determined. (More information may be included outside the disclosure box–for example, in a footnote.)

Grace period for repayment of balances for purchases

The number of days you have to pay your bill in full without triggering any finance charges. With most plans, the grace period applies only to purchases; cash advances and balance transfers may start accruing interest immediately.

Method of computing the balance for purchases

The method that will be used to calculate your outstanding balance if you carry over a balance and will pay a finance charge.

Annual fees

The annual fee (or other periodic fee) the issuer charges for you tohave the card. You may have to pay this fee even if you never use the card.

Minimum finance charge

Any minimum or fixed finance charge that could be imposed during abilling cycle. A minimum finance charge usually applies only when a finance charge is imposed, that is, when you carry over a balance.

Transaction fee for cash advances

Any charge imposed when you use the card for a cash advance. If the card charges transaction fees for purchases, these fees will also be stated here.

Balance-transfer fee

A fee for transferring balances from another card to this card, if any.

Late-payment fee

The fee imposed if your payment is late, if any.

Over-the-credit-limit fee

The fee imposed if your charges exceed the credit limit set for your card, if any.

Cracking the Credit Code

Glossary of Credit Terms

Annual fee

A flat, yearly charge similar to a membership fee

Annual percentage rate (APR)

A measureof the cost of credit expressed as a yearly rate. Many credit card plans charge different APRs for credit used in different ways–for example, one APR for purchases, another for cash advances, and still another for balance transfers. Some plans may increase the APR if a payment is late.

Cash-advance fee

A fee charged if you obtain a cash advance. This fee is in addition to the interest rate charged on the amount of the advance.

Finance charge

The dollar amount you pay to use credit. Besides interest costs, the finance charge may include other charges such as cash-advance fees.

Grace period

A period of time, often about 25 days, during which you can pay your credit card bill without incurring a finance charge. Under nearly all credit card plans, the grace period applies only if you pay your balance in full each month. It does not apply if you carry a balance forward. Also, the grace period usually does not apply to cash advances, which may begin accruing interest from the day of the transaction.

Interest rate

A measure of the cost of credit, expressed as a percent. For variable-rate credit card plans, the interest rate is explicitly tied to another interest rate, such as the prime rate or the Treasury bill rate. If the other rate changes, the rate on you card will, too. The interest rate on fixed-rate credit card plans, though not explicitly tied to changes in other interest rates, can also change over time. The card issuer must notify you before the “fixed” interest rate is changed. A tiered interest rate means that different rates apply to different levels of the outstanding balance (for example, 16% on balances of $1 – $500; 17%on balances above $500).

Late-payment charge

A charge imposed when your payment is late. If your payment arrives after the grace period, you may be charged both a finance charge (the interest on your outstanding balance) and a late-payment charge. Some card issuers may also impose a penalty rate if you have more than one late payment within several months.

Over-the-limit fee

A fee imposed when your charges exceed the credit limit set on your card.

Penalty rate

The rate that applies under specific circumstances set out by the card issuer. For example, if you make 2 late payments within 6 months, a card issuer may have a policy of raising the interest rate.

Periodic rate

The rate you are charged each billing period. For most credit card plans, the periodic rate is a monthly rate, calculated by dividing the APR by 12. For example, a credit card with an 18% APR has a monthly periodic rate of 1.5%.

You can find listings of credit card plans, rates, and terms on the Internet, in personal finance magazines, and in newspapers.

The following federal agencies are responsible for enforcing the federal Truth in Lending Act, the law that governs disclosure of terms for credit cards. Questions concerning compliance by a particular financial institution or credit card issuer should be directed to the institution’s regulatory agency.

Federal Reserve Board

Division of Consumer and Community Affairs

Mail Stop 801

Washington, DC 20551

(202) 452-3693

(regulates state banks that are members of the Federal Reserve System)

Comptroller of the Currency

Office of the Ombudsman

Customer Assistance Unit

1301 McKinney Street, Suite 3710

Houston, TX 77010

1 (800) 613-6743

(regulates banks with “national” in the name or “N.A.” after the name)

Federal Deposit Insurance Corporation

Compliance and Consumer Affairs

550 17th Street, NW

Washington, DC 20429

(202) 942-3100 or 1 (877) 275-3342

(regulates state-chartered banks that are not members of the Federal Reserve System)

Office of Thrift Supervision

Consumer Programs

1700 G Street, NW

Washington, DC 20552

(202) 906-6237 or 1 (800) 842-6929

(regulates federal savings and loan associations and federal savings banks)

National Credit Union Administration

Office of Public and Congressional Affairs

1775 Duke Street

Alexandria, VA 22314-3428

(703) 518-6330

(regulates federally chartered credit unions)

Federal Trade Commission

Consumer Response Center

6th and Pennsylvania, NW

Washington, DC 20580

877-FTC-HELP – toll free (877-382-4357)

(regulates finance companies, stores, auto dealers, mortgage companies, and credit bureaus)

Every six months the Federal Reserve System surveys the terms of credit card plans offered by financial institutions and publishes a report of the findings. The report includes information from the largest credit card issuers in the country as well as other financial institutions that wish to participate in the survey. The credit terms shown in the accompanying list are as of August 2001 and are subject to change. You should contact issuers for current rates and to learn aboutother credit card plans.

Codes Used in the List of Plans

Availability

Refers to availability of card to consumers

N = Nationally

R = Only in selected states

State abbreviation = Only in state specified

Type of Pricing

F = Fixed

V = Variable

T = Tiered, with different periodic rates for different levels of outstanding balance. Rate shown applies to the lowest of the balance tiers.

Index

The interest rate on variable-rate plans is based on an index. The codes shown in the list of plans correspond to the following indexes:

1 = Prime rate

2 = One-month Treasury bill rate

3 = Three-month Treasury bill rate

4 = Six-month Treasury bill rate

5 = One-year Treasury bill rate

6 = Federal funds rate

7 = Cost of funds to card issuer

8 = Federal Reserve discount rate

9 = Other

0 = Not applicable.

Other Features

Credit card issuers may add enhancements or other features to the plan without charging extra fees. These enhancements may include cash rebates, purchase protections, warranty guarantees, travel accident or automobile rental insurance, discounts on goods and services, and incentives for use such as frequent flyermiles.

1 = Rebates on purchases

2 = Extension of manufacturer’s warranty

3 = Purchase protection/security

4 = Travel accident insurance

5 = Travel-related discounts

6 = Automobile rental insurance

7 = Non-travel-related goods and services

8 = Credit card registration

9 = Reduced introductory interest rate available

10 = Other, not specified

N.R. = Not reported.